BRK Buys TMHC - What Does It Mean?

1 June 2026

Greg Abel, the new CEO of Berkshire Hathaway, didn’t waste any time in making his first deal after succeeding Warren Buffet. Berkshire Hathaway announced the acquisition of Taylor Morrison Home Corporation at an enterprise value of USD8.5 billion (USD6.8 billion plus USD1.7 billion of assumed debt).

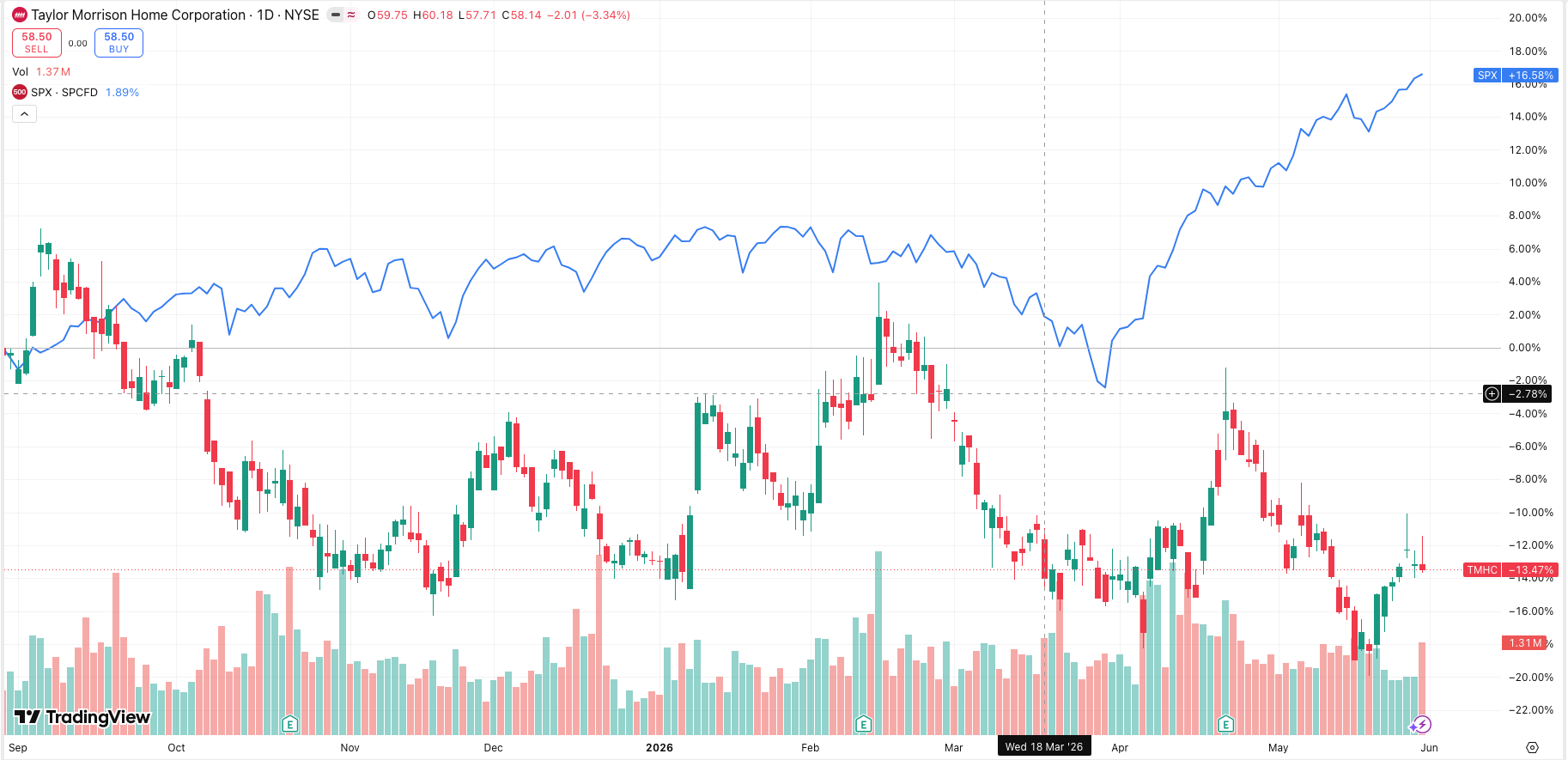

The deal itself sticks to the Berkshire mantra of “it is far better to buy a wonderful company at a fair price than a fair company at a wonderful price." One can see from the chart that TMHC has underperformed the S&P 500 - this sets up the fair price criteria that is so important to Berkshire Hathaway.

What is more important concerns the underlying assumptions and reasons that Abel pulled the trigger on this deal. One of the main underlying deal drivers is an opinion that this great home building business (America’s Most Trusted Builder - since 2016 according to Lifestory Research; and one of Fortune’s Most Admired Companies 2026) can benefit from interest rate cut optionality from the Federal Reserve.

For the Philippines, this shift in the world’s most important interest rate can act as a meaningful support for inflation control, the value of the peso, and activity in real estate and construction — provided the U.S. economy achieves a soft landing rather than a sharp downturn.

The transmission works through several linked channels. When U.S. rates ease, global investors often become more willing to hold assets outside the dollar. This can strengthen the peso against the dollar, reduce the cost of imported goods and fuel, and give the Philippine central bank more room to pause or ease its own policy rate. Lower global borrowing costs also tend to support demand for property and the financing of construction projects. These effects unfold over time in first-, second-, and third-order waves rather than overnight.

The U.S. rate path implied by the deal creates breathing room for Philippine inflation management.

The Philippine central bank raised its main policy rate to 4.5 percent in April 2026 after inflation rose above the upper end of its 3 percent target band, reaching around 7.2 percent in recent readings. Much of the pressure has come from global oil and fertilizer prices tied to international events. A gradual decline in U.S. rates reduces upward pressure on the dollar and on commodity prices priced in dollars. This lowers imported inflation over time.

In the first order, the peso tends to strengthen or stabilize against the dollar, directly cutting the peso cost of oil, food imports, and other goods. In the second order, lower imported inflation reduces the risk that price pressures become self-reinforcing through wage demands or business pricing. In the third order, the central bank gains credibility and flexibility: it can hold its rate steady or begin modest easing without fear of reigniting inflation, supporting broader economic activity.

If U.S. easing occurs because the American economy is weakening sharply rather than normalizing, global risk appetite could fall. Capital could flow out of emerging markets, pressuring the peso and forcing the Philippine central bank to keep rates higher for longer to defend the currency. That scenario would turn the signal from Berkshire into a net negative rather than a tailwind. Current market pricing and Federal Reserve projections still point more toward a soft-landing path than a hard landing, but the distinction matters enormously for the Philippines.

The peso stands to benefit from improved capital-flow dynamics.

A lower U.S. rate environment typically narrows the interest-rate gap that has favored dollar assets. Investors seeking yield or diversification become more open to Philippine government bonds, stocks, and direct investments. This supports demand for the peso. Remittances from overseas Filipino workers, already a major inflow, become more valuable in local currency terms when the peso strengthens.

First-order effect: the exchange rate moves in a more favorable direction or experiences less volatility. Second-order effect: imported inflation falls further and the central bank’s foreign-exchange reserves face less pressure. Third-order effect: improved sentiment encourages both foreign portfolio inflows and domestic investment, creating a virtuous circle for growth and asset prices.

The current level of the peso around 61 to 62 per dollar already reflects some of these global pressures. A sustained move lower in U.S. rates would likely exert gradual upward pressure on the peso’s value, all else equal. The risk is that any U.S. easing driven by recession fears could trigger a broad sell-off in emerging-market currencies, including the peso, overwhelming the positive differential effect.

Real estate and construction stand to gain from cheaper and more available financing.

Property markets in the Philippines have shown resilience in offices and certain housing segments, yet overall construction activity is forecast to decline modestly in 2026 because of project delays, softer foreign investment, and higher material costs. Lower global interest rates ease the cost of borrowing for developers and for home buyers who finance purchases. They also improve the relative attractiveness of Philippine real estate for both domestic buyers and foreign capital.

First-order effect: mortgage rates and developer financing costs stop rising or begin to edge lower, supporting demand for residential units and pre-selling activity. Second-order effect: stronger demand lifts property prices modestly and improves absorption rates, particularly in well-located mid-market and affordable segments. Third-order effect: renewed construction activity supports employment in the sector, related industries such as cement and steel, and government revenues from permits and taxes. Office and industrial segments tied to the business-process and logistics sectors also benefit indirectly from better overall economic sentiment.

If lower U.S. rates coincide with weaker global growth that reduces demand for Philippine exports or business-process services, the positive effect on real estate could be muted or delayed. Rising local material costs or regulatory delays in project approvals could also blunt the transmission. The sector most sensitive to financing costs — residential development and middle-income housing — would likely feel the benefit first and most clearly.

Overall, the Berkshire signal points to a net constructive backdrop for the Philippines over a two- to four-year horizon.

The acquisition reflects disciplined, long-horizon capital allocation rather than a bet on an immediate boom. It implies that the U.S. Federal Reserve will have room to ease policy gradually as inflation continues to moderate. That path aligns with the Philippine central bank’s own need to bring inflation back inside its target band without choking growth. The peso gains a helpful tailwind, real estate financing becomes marginally easier, and imported price pressures ease. These effects compound: lower inflation supports purchasing power, which supports consumption and property demand, which supports construction and employment.

The transmission is not automatic or guaranteed. It depends on the U.S. achieving a soft landing rather than a recession, on the Philippine central bank managing the transition skillfully, and on global commodity prices (especially oil) not spiking again. The next Federal Reserve projections, due in mid-June 2026, will provide an important update on how quickly and how far U.S. rates are expected to move.

THMC has underperformed the S&P 500 since the last quarter of 2025.